Foreword

Changing shape: Our new five-year forecasts reveal interesting patterns in prime property

.png)

Changing shape: Our new five-year forecasts reveal interesting patterns in prime property

There is no getting away from it. We have prepared this report at a time of heightened political and economic uncertainty. It would be an understatement to say it makes forecasting a tricky process. The terms of the UK’s divorce from the EU are yet to be agreed. The domestic political landscape is unsettled. There is a range of scenarios for exchange rates, interest rates, economic growth and wealth generation.

It would be easy to write off the prospects for price growth in the prime housing markets. Yet, much of the uncertainty has been present since the day of the Brexit vote. The prime housing market may not have flourished. But neither has it wasted away.

As Frances Clacy explains, the market has been price sensitive and become much more needs-based, especially given the increased costs of buying from successive stamp duty changes. But where sellers have priced stock to reflect these costs and underlying buyer caution, it has continued to sell.

Last year, we envisaged these fickle market conditions would remain until a Brexit deal was done. We pencilled that in for 2019/2020. Thereafter, we expected a return to price growth, albeit weaker than in previous cycles. That prognosis accounted for rising interest rates and a higher tax environment.

Now, we are pushing back that recovery to reflect the likelihood of an extended transition period once the Brexit deal is hammered out. We cannot be sure talks will follow this path. But a no-deal Brexit would do little for either the UK or the EU. That alone is likely to oil the wheels of negotiation.

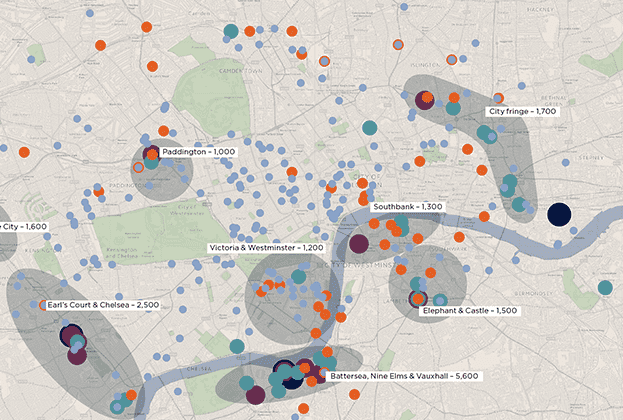

Assumptions settled, we tend to start our forecasting in central London. It is only one part of the prime housing market jigsaw, but by putting together its pieces, it is easier to tackle the rest.

As Katy Warrick says, when prime housing in central London has looked like good value, it has historically bounced back at pace. A general election in 2022 could interrupt this, while the recent announcement of further stamp duty costs for overseas buyers at the Conservative Party conference is likely to temper it.

Market conditions will change over the next five years. The patterns of the prime housing market might not be easy to predict but, taking the medium-term view, there is a place for cautious optimism.

Mat Oakley reminds us that, on the evidence of office take up, the city will remain “a major part of large companies’ European and global networks”.

So, our central London forecast has an interesting shape. In turn, that shape affects the pattern of our forecasts for other prime property in London and the UK.

9 article(s) in this publication

.png)

.png)