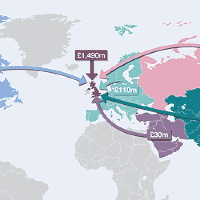

Several larger investors have demonstrated they’re willing to pay a premium on larger portfolios. This premium is driven by their need to allocate investment capital, achieve target scale / returns and secure an income stream quickly and efficiently.

Our tracking of deals suggests that these premiums tend to kick in on deals over £150m. The precise geography, location and composition of the portfolio appears to be less important. We have observed premiums on regional, London, and recently even development funding deals where investors want to assemble a large-scale pipeline quickly.

Blended yields paid for portfolios ranged from 4.6% to 5.8% over the last two years, based on our analysis of all major portfolio trades. The portfolio premium in these deals represents a yield shift of 10 to 85 basis points relative to how those schemes would be valued individually, or 38 bps on average. Premiums are particularly high for stabilised stock with a well-established cash flow.

This is because investors tend to value portfolios on an IRR basis, targeting ungeared returns of 6–7% and geared returns of 11–12%. Acquiring a portfolio quickly, even at a premium, allows investors to meet these targets much faster than through many years of organic growth.

.png)

.png)

.png)