As open market rents continue to grow, particularly in markets where demand for rental property exceeds supply, fewer properties will be affordable to those reliant on LHA to pay their rent. After only two years some large differences have opened up between the LHA rates and what they would be had they moved in line with the 30th percentile. The largest differences are where rents have risen most, mainly the South East and London.

Where housing benefit isn’t enough to pay the rent, the difference has to be made up by tenants from other income. In South West Herts, where current two bed LHA is 86% of the 30th percentile, this could cost a household £144 per month. But in Bedford, where current two bed LHA is also 86% of the 30th percentile, the cost to a household may be closer to £96.

The maps (Figures 3 to 7) show the percentage difference between the 30th percentile and the 2017 LHA rate. The gaps are greatest in the south, as a general rule, where the cash differences will also be greatest as rents are higher.

This is likely to be a consequence of greater demand in these markets, relative to supply, and higher rental growth. For the largest and smallest properties, the patterns are less clear, perhaps reflecting volatility in the data measuring fairly small markets.

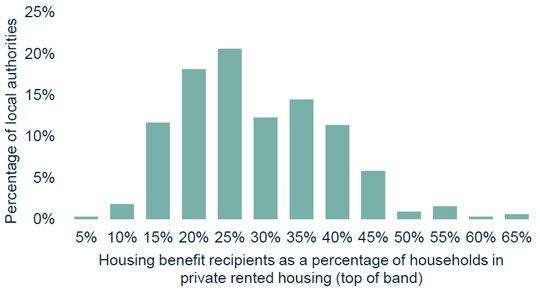

Half of all local authorities have more than 25% of private rented households claiming housing benefit. But even if LHA was still at the 30th percentile, only 30% of properties would be affordable to them unless they top up their rental payments with other income. With LHA frozen, ever fewer properties will be available to people reliant on housing benefit unless they are able to top up their rents.

This has implications for future market rent growth in locations where large proportions of rental households are reliant on housing benefit. In eight local authorities across England, more than 50% of private rented households are in receipt of housing benefit. Some stock may see limited rental growth as the amount of money households have for rent is fixed.

Where there are alternative sources of demand, benefit-reliant households will lose out. In the absence of any alternative demand, private landlords may choose to sell up rather than put up with low levels of rental growth.

.png)

.png)

.png)

.png)

.png)