(1).jpg)

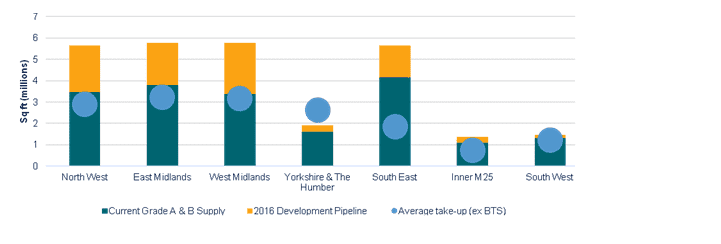

On paper the North West's industrial development pipeline looks healthy: 2.2 million sq ft (204,380 sq m) of new space is due to be delivered across 11 schemes this year. However, although this is the second largest pipeline of any UK region, it will still not be enough to absorb anything close to last year's record-breaking take-up of 4.56 million sq ft (423,324 sq m), or even the longer term average take-up of 3.44 million sq ft (319,576 sq m).

Similarly, while the current supply of existing industrial stock in the North West appears relatively robust at 5.71 million sq ft (530,459 sq m), a closer look reveals that 81 per cent of this is classified as Grade B or C. In fact, much of the latter is unsuitable for occupation. Already the shortage of Grade A space is driving a sharp rise in occupier demand for bespoke units, with build-to-suit deals accounting for 48 per cent of take-up in 2015 compared with just 18 per cent in 2014.

As a result, prime industrial rents in Manchester have risen by almost 20 per cent from £5.50 per sq ft (£59 per sq m) to £6.50 per sq ft (£70 per sq m) over the last 18 months. A combination of constrained supply and increasing build costs have also driven the freehold value of industrial land up considerably and this is expected to continue throughout 2016.

.jpg)

.jpg)

.jpg)